A quick note about some negative chatter that keeps showing up in various places.

Over the past few weeks, we have seen data suggesting a softening – but not a contracting – economy.

Consider:

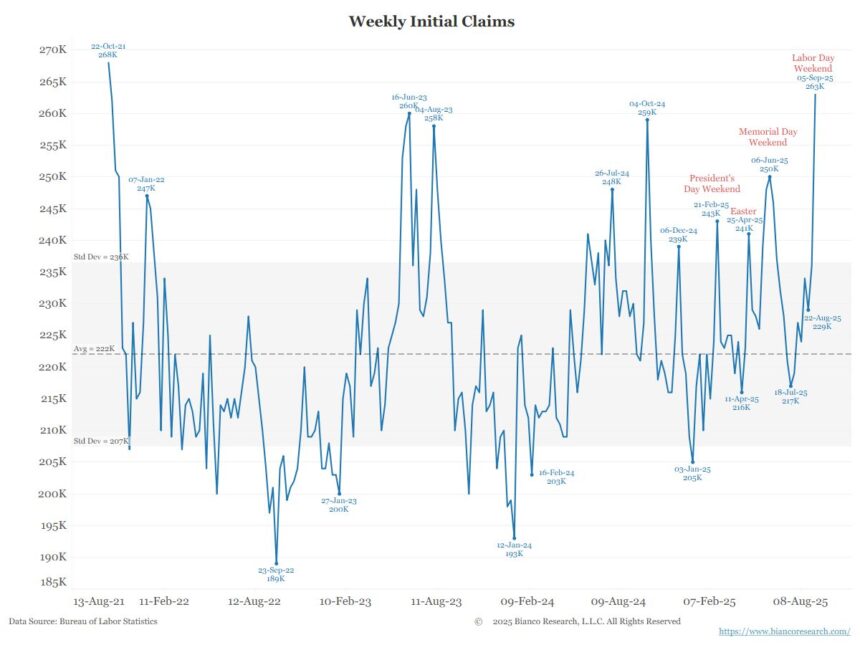

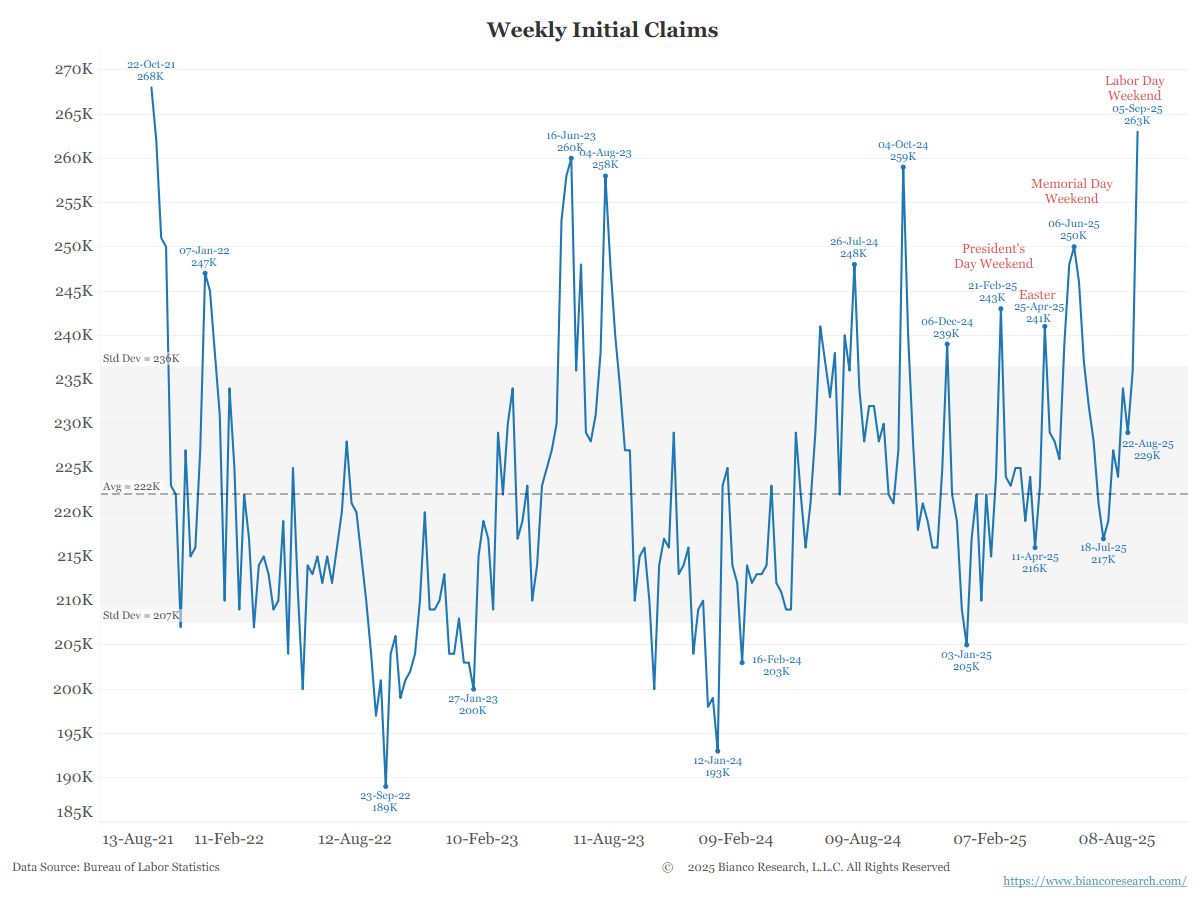

–Jobless Claims Rose Sharply Last Week to a 4-year high

WSJ: In the week through Sept. 6, jobless claims filings rose to 263,000, up from 236,000 a week earlier.–Unemployment moved up to 4.3%

Up from 3.4% in April 2023–NonFarm Payrolls gained only 22,000 in August 2025

This is the lowest increase since the pandemic.

It is easy to understand why FOMC Chair Powell has highlighted the increasing softness of the Labor Market as the primary driver of the 25-bps rate cut last week.

But in my view, it is not an immediate harbinger of a recession; rather, the weakening labor market raises the odds of a contraction sometime in 2026.

That is a probabilistic assessment, not an economic forecast. But this leads to people making the sort of claims we saw during other major dislocations:

“The Market has become detached from reality…”

I am not so sure this is correct.

Consider: The S&P500 derives almost half (41%) of its revenues from overseas. Over the past 15 years, the U.S. economy has significantly outperformed Europe and much of Asia. Credit the massive Keynesian stimulus of the first two CARES Acts under President Trump (I) and CARES Act III under President Biden, along with the 10-year Infrastructure and Semiconductor Acts (Biden) and the Tax Cuts (Trump II).

The 2020s have seen a shift from primarily monetary stimulus to a more fiscal-based stimulus. The outperformance of the US stock market over the past five years can be attributed to this significant stimulus.

This stimulus also deserves some (but not all) of the blame for the global surge in inflation from 2021-2023.

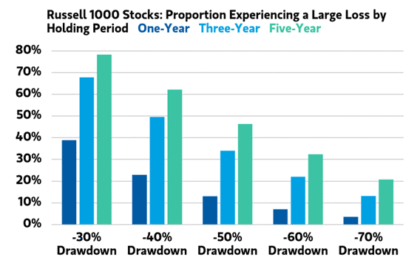

Back to stocks: Gains in EAFE markets underperformed the SPX since the 2009 GFC lows; if the US falters, does this automatically mean the US markets have a crash? Maybe, maybe not. It really depends upon a) whether the U.S. economy is decelerating or contracting.

So far, we see softening hiring but little increase in layoffs. The US has a structural shortage of workers, particularly in trades, STEM fields, construction, agriculture, healthcare, and hospitality services. One scenario is the U.S. GDP slows to under 2%, but does not enter a recession.

If a US economic slowdown occurs as Europe and Asia emerge from their moribund stasis, we could see revenues and profits in the SPX continue to grow, albeit at a more subdued pace. The wild card remains Tariffs (See our MiB with Neal Katyal), which the OECD says will present an economic hit to Global GDP in 2026.

All of these varied outcomes are possible; I am not sure any of them are probable. All are certainly realistic possibilities…

Previously:

Crosscurrents (August 25, 2025)

Maybe Mr. Market Is Rational After All… (August 7, 2020)

What if Dunning Kruger Explains Everything? (February 27, 2023)

Who Is to Blame for Inflation, 1-15 (June 28, 2022)

See also:

MiB Special Edition: Neal Katyal on Challenging Trump’s Global Tariffs (September 3, 2025)